How to Explain Trial Rights to Your Clients

Trial rights can get a little tricky, even for veteran agents. Imagine how difficult they can be for your clients to understand! The 2016 Choosing a Medigap Policy Guide explains trial rights really well. Follow along as we dissect the publication so you, and your clients, can feel more comfortable with the right to buy!

What are Trial Rights?

According to page 21 of the 2016 Choosing a Medigap Policy Guide, a trial right allows you to test out a Medicare Advantage plan and still purchase Medigap (Medicare Supplement) coverage if you decide you don’t want the MA policy.

Explaining it to Your Client

Mrs. Smith, you may qualify for a trial right. This means you can try the Medicare Advantage plan you were interested in, but if you change your mind, we can go ahead and write you a Medicare Supplement plan instead. How does that sound?

Remember to remain compliant when conducting a Medicare Advantage sale! It is a serious violation to market part C & D plans door-to-door and over the phone. You are also not allowed to bring up MA unless the client has expressed interest on the Scope of Appointment form.

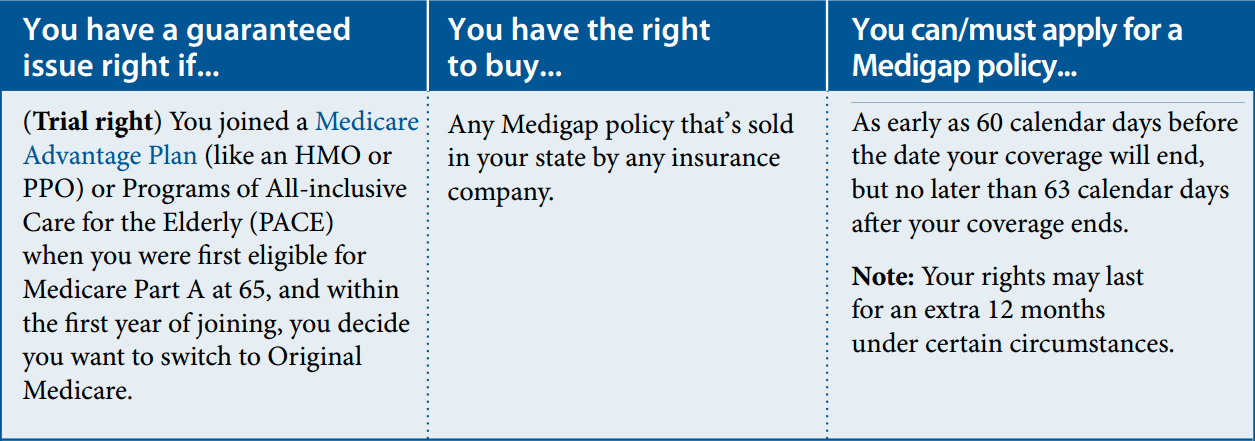

When Does One Have Trial Rights?

Page 23 of the 2016 Choosing a Medigap Policy Guide gives two trial right situations in which federal law gives you the right to buy a policy and explains which policy you can purchase.

Situation 1

“You joined a Medicare Advantage Plan (like an HMO or PPO) or Programs of All-inclusive Care for the Elderly (PACE) when you were first eligible for Medicare Part A at 65, and within the first year of joining, you decide you want to switch to Original Medicare.” (Pg. 23, Medicare-Medigap-Guide)

What You Can Buy

“Any Medigap policy that’s sold in your state by any insurance company.” (Pg. 23, Medicare-Medigap-Guide)

When You Can/Must Apply

“As early as 60 calendar days before the date your coverage will end, but no later than 63 calendar days after your coverage ends.” (Pg. 23, Medicare-Medigap-Guide)

(Image taken directly from page 23 of the 2016 Choosing a Medigap Policy Guide)

(Image taken directly from page 23 of the 2016 Choosing a Medigap Policy Guide)

Explaining it to Your Clients

Mr. Thomas, I understand your frustration with your Medicare Advantage policy. Fortunately, since you joined the plan when you were first eligible, and it’s been less than a year, you can apply for a Medicare Supplement plan. Would you like me to explain your options?

Situation 2

“You dropped a Medigap policy to join a Medicare Advantage Plan (or to switch to a Medicare SELECT policy) for the first time, you’ve been in the plan less than a year, and you want to switch back.” (Pg. 23, Medicare-Medigap-Guide)

What You Can Buy

“The Medigap policy you had before you joined the Medicare Advantage Plan or Medicare SELECT policy, if the same insurance company you had before still sells it. If your former Medigap policy isn’t available, you can buy Medigap Plan A, B, C, F, K, or L that’s sold in your state by any insurance company.” (Pg. 23, Medicare-Medigap-Guide)

When You Can Apply

“As early as 60 calendar days before the date your coverage will end, but no later than 63 calendar days after your coverage ends. ” (Pg. 23, Medicare-Medigap-Guide)

(Image taken directly from page 23 of the 2016 Choosing a Medigap Policy Guide)

Explaining it to Your Clients

Not a problem, Ms. Williams. If you liked the Medicare Supplement you had before more then the Medicare Advantage you have now, we can switch you back. Is that something you want to do?

Well, we can’t put you back on the plan you had before because that company doesn’t offer it anymore. You can still switch back to a Medigap policy, but we will need to do some research to get you the best benefits in your price range. How does that sound?

If you don’t have the 2016 Choosing a Medigap Policy Guide, we suggest getting your hands on a physical copy! It’s never a bad idea to back up your statements with proof and showing your clients these pages from a trusted CMS Publication will do just that!